Social Security and Medicare are cornerstones of what is sometimes called America’s “safety net.”

These federal programs were never intended to fund a lavish retirement lifestyle or the most expensive health-care services. Rather, they were created to provide a basic level of support for older people who have left the workforce. Although the programs have been expanded to include other beneficiaries, their primary focus is on older Americans.

Despite the limited nature of Social Security and Medicare, the benefits can be invaluable. Whether you are already eligible or will be in the future, it might be wise to consider the basic options and potential strategies that could help you obtain the benefits that are most appropriate for your personal situation. Here’s a brief overview of both programs.

Most of the information contained herein comes from the Social Security Administration and the Centers for Medicare & Medicaid Services. More information can be found at socialsecurity.gov and medicare.gov.

Social Security: Supplementary Income for Older Americans

A Brief History

The Old-Age, Survivors, and Disability Insurance (OASDI) program — the of cial name of Social Security — was created as part of Franklin Delano Roosevelt’s New Deal legislation during the Great Depression.

It was signed into law in 1935 and is now the federal government’s largest single program.

Social Security benefits were intended to “insure the essentials” for retired older workers by paying them a steady, modest income. The program was designed to be a pay-as-you-go system, which means payroll taxes collected from workers and employers are used to fund payments for current retirees.

Over the years, Social Security has been expanded to include dependents and survivors of retired workers, disabled workers, and dependents of disabled workers. According to the 2015 Annual Report of the Board of Trustees, at the end of 2014, the combined OASDI program was providing $870 billion in benefits to more than

59 million people:

- 39 million retired workers & 2.9 million dependents

- 6.1 million survivors of deceased workers

- 9 million disabled workers & 2 million dependents

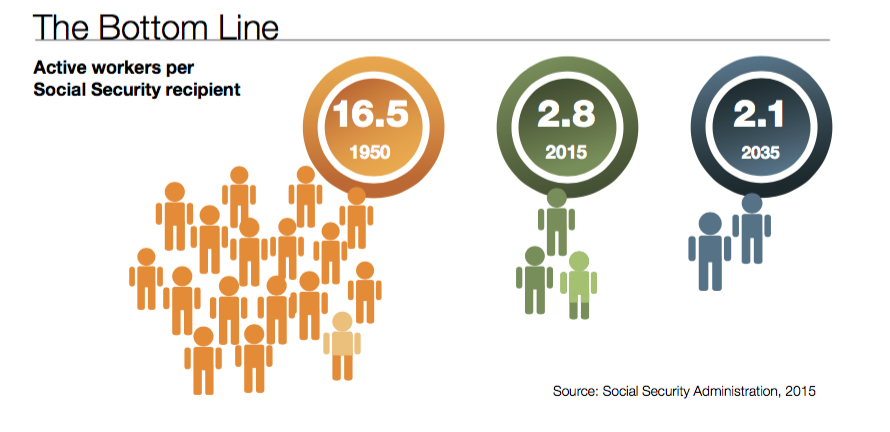

Challenges of an Aging Population

As the population ages, the ratio of workers (paying into Social Security) to retirees (receiving benefits) continues to fall. In most years prior to 2010, Social Security had annual surpluses, but they were not set aside to pay for future benefits. Rather, they were spent as part of the federal government’s general revenues, and “IOUs” were issued to the Social Security Administration in the form of financial accounts. These accounts are often referred to as the Social Security “trust funds.”

Since 2010, Social Security outlays have consistently exceeded tax revenues. The program’s six- member Board of Trustees project that outlays will continue to exceed revenues on a regular basis. This means that Social Security will continue tapping the interest on trust fund assets to cover benefits.

When you include the trust funds, Social Security should have sufficient resources to pay 100% of scheduled retiree benefits until 2034. Once the trust fund reserves are exhausted, payroll tax revenues would be sufficient to cover only about 79% of scheduled retiree benefits (this percentage will decline to 73% by 2089, based on the current benefit formula).

Eligibility

Workers who have accumulated a minimum of 40 work credits, which is 40 fiscal quarters or about 10 years of work, are entitled to receive Social Security retirement benefits. The benefit is based on an average of the highest 35 years of earnings in the workforce (during which payroll taxes were paid).

Spouses of eligible workers can collect Social Security benefits regardless of whether they worked or not. Even the unmarried ex-spouse of an eligible worker may be entitled to Social Security benefits based on the former spouse’s work record if they were married for at least 10 years.

Claiming Ages

You are eligible to receive your “full” Social Security benefit when you reach your “full retirement age.” In the past, this was age 65, but now it ranges from 66 to 67 depending on year of birth.

The earliest you can claim retired worker benefits is age 62, but if you do so the monthly benefit is permanently reduced. For each month you wait to claim benefits after age 62, your bene t increases slightly, so that at full retirement age you are entitled to 100% of your full retirement benefit.

You can delay claiming Social Security up to age 70. For each year you wait after reaching full retirement age, your benefit will increase by about 8%.

Spousal Benefits

Spouses are entitled to receive a benefit based on their own earnings history or a spousal benefit that could be as high as 50% of the other spouse’s full benefit amount.

To receive a spousal benefit, you must be age 62 or older, you must have been married for at least one year, and your spouse must be receiving Social Security benefits. A spousal benefit claimed at your full retirement age would be equal to one-half of your spouse’s Primary Insurance Amount. If you elect to receive a spousal benefit before you reach full retirement age, you will receive a permanently reduced benefit, unless a qualifying child is being cared for. The reduction amount is based on your age when claiming the spousal benefit.

An unmarried, divorced spouse may also be eligible to collect retirement benefits based on a former spouse’s work record if they were married for at least 10 years. These benefits have no effect on the former spouse’s benefits or on his or her subsequent spouse’s benefits.

Once you file for Social Security, you will be “deemed” to be applying for the maximum benefit to which you are entitled — whether it’s your own retired worker benefit or a spousal benefit. You will not be able to switch from one benefit to the other.

The new deeming rules for spousal benefits will not affect married people who turned 62 before the end of 2015. This means they are still eligible to file for spouse-only benefits upon reaching full retirement age and earn delayed retirement credits on their own work records.

Survivor benefits, however, are not affected by these rules, so an eligible widow or widower can switch from a spousal or worker benefit to a survivor benefit (or vice versa).

Survivor benefits

Widows and widowers have dual entitlements under Social Security: benefits based on their own earnings history or survivor benefits based on the deceased spouse’s earnings record.

To claim a survivor benefit, you must have been married for at least nine months (or for at least 10 years if you are a surviving divorced spouse). The survivor benefit amount is based on the earnings record of the spouse who died. The more the worker paid into the program, the higher the survivor benefit would be.

Unlike spousal benefits, survivor benefits reflect any delayed retirement credits the deceased spouse may have earned. You are eligible for a reduced survivor benefit as early as age 60 or for a full survivor benefit (100% of the deceased’s worker benefit amount) once you reach full retirement age. Surviving disabled spouses and those with young children may have additional options.

- Warning: If you remarry before reaching age 60, you will forfeit your late spouse’s Social Security benefits while you are married. If you remarry after age 60, you continue to qualify for survivor benefits based on your deceased spouse’s work record.

Changes to Social Security Claiming Strategies

The Bipartisan Budget Act of 2015 effectively eliminated two claiming strategies used by some married couples to enhance benefits, and made other changes to Social Security.

File and Suspend

This “voluntary suspension” strategy was typically used by married couples to enhance their combined lifetime benefits. Upon reaching full retirement age, one spouse would file for worker benefits and immediately suspend them, which enabled the individual to earn delayed retirement credits (while often continuing to work) and his or her spouse to collect a spousal benefit.

New rules: The ability to “ file and suspend” benefits upon reaching full retirement age is still available, but no benefits will be paid to you or others during the suspension period.

- Some married couples who turned 66 before the new rule’s effective date (April 30, 2016) may have had time to take advantage of the original claiming strategy.

Restricted Application

By filing a “restricted application” for a spouse-only Social Security benefit upon reaching full retirement age, some married individuals have been able to delay claiming benefits on their own work records while receiving a spousal benefit. Meanwhile, their own worker bene t would increase in value (about 8% annually), up to age 70.

New rules: Only individuals who turned 62 before the end of 2015 can continue using the “restricted application” for a spouse-only benefit and later claim their own worker benefit.

Those born in 1954 and later who are eligible for a worker benefit and a spousal benefit will receive whichever amount is higher when they file for Social Security.

“Do Over” or “Reset”

If you regret taking a permanently reduced Social Security benefit before reaching full retirement age, you can apply to withdraw benefits within 12 months of making the original claim for benefits. However, you must repay all benefits you and your spouse have received. This option is available only once in your lifetime.

- The “do over” strategy was not changed by the Bipartisan Budget Act of 2015.

“Start, Stop, Restart”

If you have already started receiving benefits and would prefer to stop them in order to receive higher benefits later, you can ask Social Security to suspend future benefits and restart them at a later date. To request this action, you must have reached full retirement age.

- Keep in mind that your spouse cannot receive spousal benefits during the time when your benefits are suspended.

How Working Affects benefits

If you plan to continue working, it may be wise to delay claiming Social Security benefits until you reach full retirement age.

If you claim benefits prior to full retirement age and continue to work, one dollar in benefits will be deducted for each two dollars earned above the annual limit ($15,720 in 2016).

In the calendar year in which you reach full retirement age, one dollar in benefits will be deducted for each three dollars you earn above a higher annual limit ($41,880 in 2016) until your birthday month.

Once you reach full retirement age (66 to 67, depending on birth year), any wages earned through employment will not affect your Social Security benefit.

Of course, you must pay Social Security and Medicare payroll taxes on any wages earned through employment.

If your benefits are reduced because of these limitations, your benefit will be recalculated after you reach full retirement age, and you will receive credit for any benefits you did not receive because of your earnings.

How Social Security Benefits Are Taxed

If your income exceeds certain income thresholds, you may owe federal income tax on up to 50% or 85% of your Social Security benefits.

The IRS uses your “combined income” to determine taxability of benefits. Combined income is de ned as your adjusted gross income plus any tax-exempt interest (such as interest from municipal or savings bonds) plus 50% of your Social Security benefit.

If you are married and file a separate tax return, you will probably pay taxes on all your Social Security benefits. In addition, some states may tax Social Security benefits, whereas other states may exempt them from taxation.

- About 40% of current beneficiaries pay taxes on their Social Security benefits.

Will Your Sources of Income Last a Lifetime?

At age 65, a healthy man or woman can reasonably expect to spend up to 20 or 30 years in retirement. If a couple is married, there is a 40% chance that one of them will live to age 90.

Social Security offers benefits similar to a lifetime pension. Not only does it provide a guaranteed income stream, but it also offers longevity protection, spousal protection, and even some inflation protection.

Regardless of your marital status, there are strategies that might increase the lifetime benefits you receive from Social Security. It is also important to understand how the claiming age of each spouse could affect monthly and lifetime benefits.

Maximizing Lifetime and Survivor Benefits

A married couple could potentially increase their lifetime benefits — as well as the benefits of a surviving spouse — by claiming Social Security at different ages.

This example illustrates three hypothetical claiming scenarios for a married couple, Jane and Paul (both age 62). It looks at potential monthly and lifetime benefits assuming that Paul dies at age 80 and Jane dies at age 90.

Although the couple’s combined benefits at the time of Paul’s death would be highest under Scenario 2, the third scenario would provide the highest lifetime benefits if Jane were to live to age 90. Jane’s monthly survivor benefit would be $1,500 under Scenario 1, $2,000 under Scenario 2, and $2,640 under Scenario 3 — which translates to annual amounts of $18,000, $24,000, and $31,680, respectively.

Medicare: Health Insurance for Older Americans

Medicare is the U.S. government’s health insurance program for citizens aged 65 and older, as well as some younger individuals with specific disabilities and illnesses, and families of deceased workers.

Generally, to be eligible for Medicare, you need to be age 65 and you (and/or your spouse) must have paid Medicare and Social Security payroll taxes for at least 10 years. The cost for Medicare will depend on your income, the options you choose, and the medical care you need.

There are two ways to receive Medicare coverage: Original Medicare or Medicare Advantage.

Original Medicare is divided into two parts: Parts A and B. Participants also have the option of purchasing Part D prescription drug coverage as well as Medicare Supplement Insurance (Medigap), which helps fill in coverage gaps.

Medicare Advantage (Part C) plans combine Parts A and B, offer other benefits, and often include prescription drug coverage.

- Parts A and B are administered by the federal government.

- Parts C and D and Medigap are offered by private, Medicare-approved insurance companies.

Because Medicare covers a limited amount of skilled nursing facility care (after a three-day hospital stay), there is a common misconception that Medicare will pay for long-term care. However, all costs for long-term care — assisted living, nursing home care, personal assistance at home — must be paid for out of pocket.

Medicare Coverage Options

- In 2014, Medicare covered 44.9 million people aged 65 and older and 8.9 million disabled individuals.

Medicare Enrollment

Enrolling in Medicare can be complicated, with substantial penalties for missing certain deadlines. It is important to become familiar with the enrollment process and rules, not only as you approach age 65 but also if you already have coverage.

Initial Enrollment Period

To avoid penalties, you should enroll during the initial enrollment period, which starts three months before the month you turn 65 and ends three months after the month you turn 65. Depending on when you enroll, coverage will start on the rst day of the month indicated here.

If you are receiving Social Security, you will be enrolled automatically in Medicare Parts A and B when you turn 65. If you are not receiving Social Security, you must apply for Medicare coverage.

If you are still working and have employer-provided health coverage, it makes sense to apply for Medicare Part A when you turn 65, but you don’t have to enroll in Parts B or D, and there is no penalty. The deadline for signing up for Part B (and avoiding higher premiums) is exactly eight months after your final day of employment, regardless of when health benefits end.

General Enrollment Period

If you didn’t sign up for Part A and/or Part B when you were first eligible, you can sign up between January 1 and March 31 each year. Your coverage would begin on July 1. However, you may have to pay a higher premium for late enrollment.

Late Enrollment Penalties

- Part A — If you are not eligible for premium-free Part A and didn’t sign up when you were first eligible, your monthly premium may go up 10%. You will have to pay the higher premium for twice the number of years you could have had Part A but didn’t sign up for it.

- Part B — If you did not sign up for Part B when you were first eligible, you may have to pay a late enrollment penalty for as long as you have Medicare. Your monthly premium for Part B may go up 10% for each full 12-month period that you could have had Part B but didn’t sign up for it.

Annual Open Enrollment

Medicare offers an opportunity to make changes during Open Enrollment from October 15 to December 7 each year; changes are effective on January 1. During this open enrollment period, Medicare beneficiaries can do the following:

- Change from Original Medicare to a Medicare Advantage plan and back again.

- Switch from one Medicare Advantage plan to another Medicare Advantage plan, including switching from a plan that does not offer prescription drug coverage to one that does, and vice versa.

- Join a Medicare prescription drug plan, switch from one Medicare prescription drug plan to another, or drop Medicare prescription drug coverage.

Costs Associated with Medicare

Medicare generally covers only about 60% of the cost of health-care services for beneficiaries aged 65 and older. Out-of-pocket costs may include premiums, deductibles, copays, and coinsurance. Costs vary depending on the coverage you choose and the medical services you use.

Medicare Premiums

Part A is generally premium-free if you or your spouse paid Medicare payroll taxes for at least 10 years. If not, you may pay up to a $411 monthly premium in 2016.

Part B premiums are based on modified adjusted gross income (AGI), as reported on your IRS tax return two years before the year for which Medicare premiums are paid. (See facing table.)

Part C (Medicare Advantage) premiums vary by plan.

Part D premiums also vary by plan, but higher-income individuals must pay an extra charge in addition to the plan’s regular premium.

Medigap

If you are enrolled in Original Medicare Parts A and B, you have the option of purchasing Medicare Supplement Insurance, or Medigap, which is sold by Medicare-approved private insurers. Medigap policies are designed to help cover the deductibles and copayments that the original program doesn’t cover, but it will not pay for procedures that aren’t covered by Medicare. If you are enrolled in a Medicare Advantage plan, you don’t need (and cannot enroll in) Medigap.

- People often underestimate the potential cost of health care in retirement — even with Medicare.

Medicare Part B and Part D Monthly Premiums (2016)

(based on AGI for 2014 tax year)

Out-of-Pocket Costs

A 65-year-old couple without employer-provided health coverage could expect to pay about $245,000 for medical care during retirement, typically allocated across these three categories.*

*The $245,000 estimate for medical care does not include costs for

dental care, over-the-counter drugs, or long-term care.

**Items not covered by Medicare include vision and hearing exams, eyeglasses, and hearing aids.

The benefits you receive from Social Security and Medicare could play an important role in retirement. But it might be wise to place a greater emphasis on accumulating sufficient savings and assets to enjoy a comfortable financial future.